Unlock Success in the Real Estate Market with Avant ONE

buying a home

buying a home

Stay Ahead in the Ever-Changing Real Estate Market with Avant ONE

In the world of real estate, knowledge is your most potent asset. Staying informed is paramount, allowing you to navigate a market that evolves at the speed of light. At Avant ONE real estate, we work tirelessly to arm you with the insight you need for your next transaction.

Twelve months ago, I had forecasted a situation of escalating property prices. My prediction was built on the convergence of several factors – a tightened inventory, a massive activity boom posts the pent-up demand phase of 2020/22, and a backdrop of millions of under-built homes in the US.

Fast forward to today, and the S&P CoreLogic Case-Shiller National Home Price Index has provided some intriguing insights. Despite an anticipated increase in interest rates, this key indicator witnessed a 0.4% rise in March compared to February. Although it represents a slight dip from the 2.1% annual rate seen in February, the year-over-year index increase of 0.7% in March is not to be dismissed.

The data paints a rather interesting picture across the country. Miami led the charge with a robust 7.7% annual home-price growth, closely followed by Tampa at 4.8%. At the other end of the spectrum, Seattle saw a 12.4% annual dip in prices.

It's important to note that the Case-Shiller index operates on a two-month lag, with the March data reflecting decisions made at the beginning of the year or late 2022.

What does this mean for you? Simply put, the price readjustment across several US regions seems to be slowing down. This is happening during uncertain economic times compounded by high-interest rates. Now, envision the potential scenarios:

The equation is simple. Under-supply and surging demand equal potential price hikes – a fundamental principle from Economics 101. With high interest rates now, buying and refinancing later when rates dip could be a wise strategy.

The Spring Effect and Current Inventory Trends

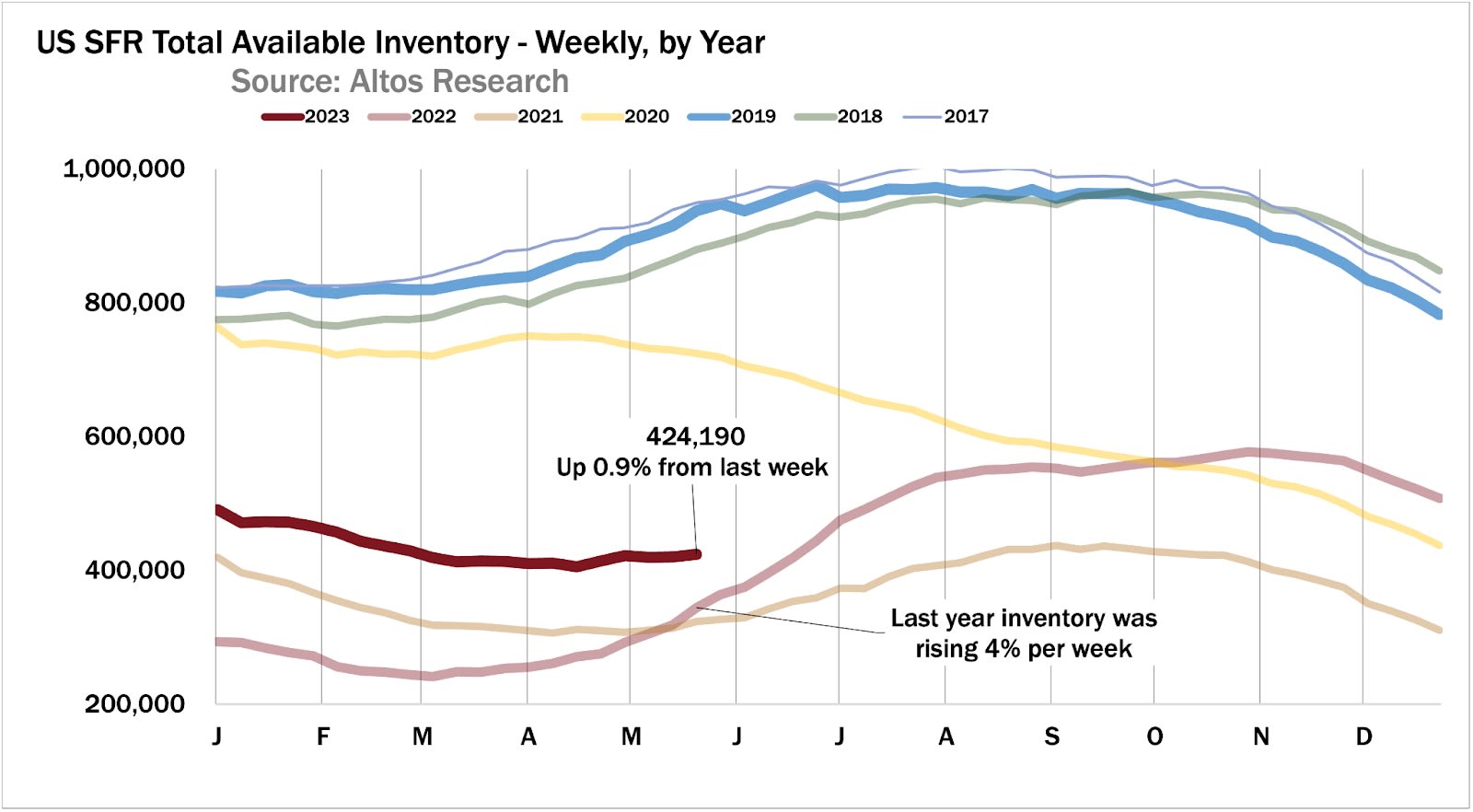

Spring has traditionally been a time of bustling activity in the real estate market. We usually witness an inventory increase as sellers prepare their homes for the summer home-buying peak. Historically, mid-February marks the low point for homes on the market. However, 2023 took a different trajectory. The low point arrived ten weeks later, in late April, thanks to a unique scenario where demand for homes exceeded the supply throughout Q1.

The chart that accompanies this section paints a vivid picture of these trends. It delineates the inventory curve of unsold single-family homes on a weekly basis, for each year. Notice how the pandemic years' inventories create the lowest lines? From May 2020 through March 2021, the market was dominated by a dearth of sellers and a ravenous buyer demand.

You can trace how last year's inventory began a swift upward climb in Q2, as mortgage rates started to ascend. This trend is captured by the light red line. Unusually, 2022 saw a second inventory growth burst in September, a direct reflection of the dramatic slowing of homebuyer demand as mortgage rates shot past the 7% mark.

By mid-May 2023, only 424,000 single-family homes were on the market nationwide, with the lowest point officially recorded in mid-April. We are now seeing a slight uptick, with the available inventory of homes for sale starting to creep up by 1% per week. This contrasts starkly with the same period in 2022, when inventory was climbing at a much brisker pace of 6% weekly.

The market, as it stands, remains a dynamic and challenging landscape. As inventory begins its slow ascent, staying informed and having a partner like Avant ONE on your side will be key to navigating your real estate journey.

Staying ahead of the curve is easier when you have a team like Avant ONE on your side. We ensure that you are armed with the knowledge and tools to navigate this complex real estate market, helping you make the right decisions at the right time.

Stay up to date on the latest real estate trends.

Wildfire Seson

Deadline Alert: June 1st for Ventura and Los Angeles County Residents - Act Now to Protect Your Home and Community!

Real estate valuation

Decoding Real Estate Metrics to Ensure Accurate Property Comparisons

Remodeling

How to Blend Style, Functionality, and Sustainability in Your Bathroom Makeover

Real Estate Industry

Understanding the Impact of NAR's Proposed Settlement on Real Estate

avant one real estate

Unveiling Opportunities in Westlake Village, Thousand Oaks, and Beyond

Trusts and Estate Planning

Protecting Assets and Beneficiaries for Future Generations

buying a home

Insider Tips from Ventura County to Los Angeles County

luxury

Unveiling the Spring and Summer Trends in Real Estate

luxury real estate selling

Exploring Your Options

You’ve got questions and we can’t wait to answer them.